Huahong Technology: H1 net profit expected to rise YoY by 301.84%-352.08% as major rare earth product prices rise

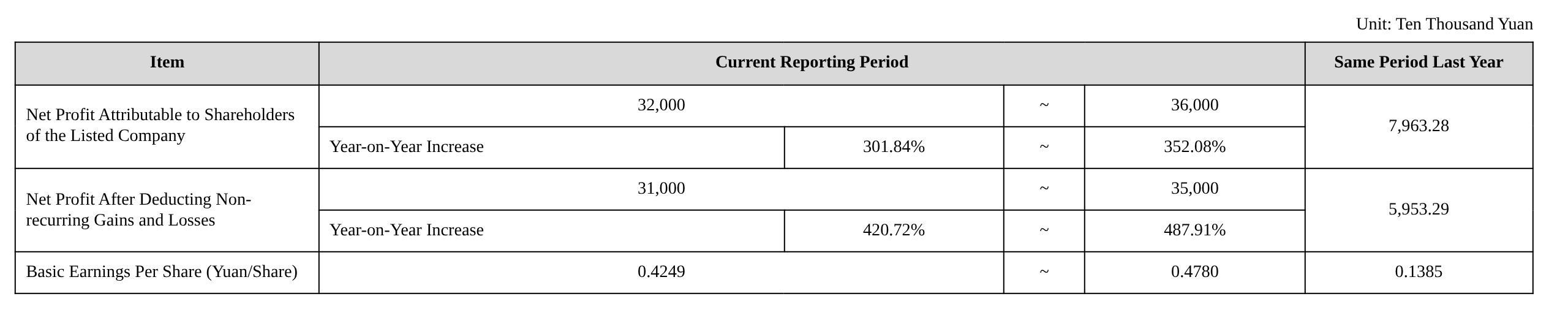

Huahong Technology’s semi-annual results forecast disclosed on the evening of July 13 shows that attributable net profit in H1 2026 is expected to be 320 million yuan to 360 million yuan, up 301.84%–352.08% YoY. As for the reasons for the performance change, Huahong Technology said: In H1 2026, driven by industry policies and improved downstream demand, prices of major rare earth products in China climbed steadily. The company’s rare earth comprehensive utilization segment seized market opportunities, fully leveraged its comprehensive advantages in capacity scale, cost control and process technology, and continuously optimized its supply, production and sales coordination and inventory management strategies, effectively driving the full release of the segment’s profitability. The company continued to deepen its rare earth industry chain layout, steadily expanding its downstream rare earth permanent magnet materials business. Driven by steady demand from end-use sectors such as NEVs, wind power and industrial automation, the segment’s business scale kept expanding, its revenue and product mix continued to improve and it became an important supplement to performance growth. A review of SMM’s Pr-Nd oxide price trend in H1 shows that the Pr-Nd oxide price stood at 609,000 yuan/mt at the start of the year, hit its H1 high of 890,000 yuan/mt by late February, a cumulative gain of up to 46.7% from the start of the year. The key driver was the supply side: spot Pr-Nd oxide supply remained tight, futures surged sharply, suppliers held back from selling amid strong bullish sentiment, and pre-holiday stockpiling purchases by metal companies pushed prices up rapidly. At the same time, supply disruptions from Myanmar ore, domestic separation plants’ production resumptions falling short of expectations and market sentiment created a combined effect of “undersupply + bullish hold-back.” From March to April, however, bearish supply-side news combined with weak demand from traditional end-use sectors pulled Pr-Nd oxide prices back quickly to around 700,000 yuan/mt. Yet the rise in China Northern Rare Earth’s concentrate prices in April, supply support from production suspensions at separation plants and export orders released under the export control extension window together drove prices to rebound slightly. From May, downstream sectors gradually entered the off-season and purchases became more cautious. From late June, the formal implementation of the Mineral Resources Law Implementation Regulations, which list rare earths as strategic minerals, and production cuts by scrap recycling enterprises due to tax invoice issues boosted Pr-Nd oxide prices again, which rebounded to 742,500 yuan/mt on June 30. Huahong Technology announced on June 30 that its controlling shareholder Jiangsu Huahong Industrial Group Co., Ltd., which holds a 32.01% stake, plans to reduce its holdings by no more than 15.0102 million shares (1.99% of total equity) through centralized bidding and block trading within three months after 15 trading days; Director and senior executive Zhu Dayong, who holds a 0.19% stake, plans to reduce his holdings by no more than 365,000 shares (0.05% of total equity) through centralized bidding or block trading within three months after 15 trading days; Director and senior executive Liu Weihua, who holds a 1.52% stake, plans to reduce his holdings by no more than 2.8 million shares (0.37% of total equity) through centralized bidding or block trading within three months after 15 trading days. Huahong Technology previously released its 2025 annual performance report, showing that in 2025, the company achieved operating revenue of RMB7.835 billion, up 40.51% YoY, reaching a three-year high. After posting losses for two consecutive years, the company successfully returned to profitability, with net profit attributable to shareholders of the parent company reaching RMB204 million, up 157.46% YoY. 1. The rare earth segment seized the industry opportunity, acting as the "ballast stone" and "engine" for the turnaround. In 2025, the global rare earth market experienced a major shift in the supply-demand pattern. Driven by surging downstream demand from sectors such as new energy and robotics, combined with rigid supply-side constraints, rare earth product prices continued to rise, with the cumulative annual price increase for core products like Pr-Nd oxide exceeding 35%. The company's Rare Earth Resource Comprehensive Utilization Division keenly captured this industry opportunity, made accurate assessments, and acted accordingly: the company kept pace with the market, optimized procurement and sales strategies, and maximized product value during the price upcycle. Technological transformation yielded results and capacity was released: the previously completed technological transformation and capacity expansion projects at Xintai Technology and Jiangxi Wanhong reached full production, with annual capacity for rare earth oxides stabilizing at 12,000 mt, significantly releasing economies of scale. The company tapped internal potential to reduce costs and enhance efficiency: by optimizing process flows, production costs were strictly controlled and recovery rates were improved. During the reporting period, the company's rare earth resource comprehensive utilization business recorded strong production and sales performance with rising volumes and prices, contributing core profits to the company. 2. All business segments collaborated to build a diversified support structure. While the rare earth resource comprehensive utilization segment led the way, other segments also achieved strong operating results, creating a favorable situation of "blossoming in multiple areas and developing in synergy": Rare Earth Magnetic Materials Segmentachieved "dual improvement in volume and quality," with production capacity steadily released across various production sites, providing strong support for market expansion and order fulfillment. High-performance magnetic material products were successfully introduced into the supply chain systems of multiple first-tier NEV automakers, with order scale continuing to expand and client quality and business mix continuously optimized. Construction of the key Baotou production site is progressing in an orderly manner and is planned to enter trial production in Q2 2026, laying a critical foundation for doubling magnetic material capacity.Elevator Parts Segment:The traditional business seized the policy dividends from the "program of large-scale equipment upgrades and consumer goods trade-ins," rapidly responding to domestic demand for elevator installation and retrofitting. Through refined production scheduling and efficiency gains, total annual production grew by over 20% YoY. The segment steadily expanded its second growth curve, with customer acquisition and product development activities for emerging businesses such as automotive electronics and energy storage progressing on schedule. At the same time, the division's "going global" process accelerated, closely following market trends and customer needs. Renewable Resource Equipment Segment: In the face of profound industry changes and intense market competition, the business division continued to increase investment in new product R&D and accelerated its deployment in markets outside China, striving to secure survival and development amid fierce competition. Internally, it focused tightly on cost reduction across supply, production, and sales to enhance operational quality. In the renewable resource operations segment, the end-of-life vehicle dismantling and steel scrap processing businesses constantly explored more diverse and flexible business models, and introduced specialized teams to improve operational quality and efficiency. In 2025, the company's total volume of end-of-life vehicle recycling and dismantling reached a record high. The business models continued to mature, internal management was consistently optimized, and industry synergies were accelerated, laying a foundation for future business development. In 2025, the company also achieved notable results in cross-segment industry synergies. The industrial linkages between the Magnetic Materials Business Division and the Rare Earth Business Division, the industry sharing between the Elevator Business Division and the Magnetic Materials Business Division, and the upstream-downstream resonance between the operations segment and the Rare Earth Business Division demonstrated the wisdom and commitment of the company's entire management team. Regarding the company's main business operations, HuaHong Technology's 2025 Annual Report disclosed: The company has consistently upheld its corporate mission of "Serving the Circular Economy, Creating a Green Life" and steadfastly adhered to its corporate spirit of "Striving, Fact-Based, Innovation, and Dedication," committing to becoming a renewable resource processing equipment manufacturer and a comprehensive resource recycling and utilization operator serving global markets. The company actively deployed renewable resource operation businesses, building a circular economy industry chain centered on end-of-life vehicle recycling and dismantling, extending downstream to the comprehensive utilization of steel scrap, rare earth recycling materials, and other metallic and non-metallic resources, while continuously exploring possibilities for expansion into related industries such as high-end manufacturing and smart manufacturing. During the reporting period, the company's main business was divided into four major segments: "Renewable Resource Equipment and Operations," "High-End Manufacturing of Elevator Parts," "Comprehensive Utilization of Rare Earth Resources," and "Rare Earth Magnetic Materials." HuaHong Technology's corporate development strategy and business plan announced in its 2025 Annual Report indicate: The company's overall development approach is as follows: strengthen product upgrades and technological innovation in renewable resource processing equipment to further consolidate its leading position in the renewable resource processing equipment industry; actively deploy renewable resource operation businesses, vigorously develop the end-of-life vehicle recycling and dismantling business, and use this as a main line to expand the comprehensive recycling and utilization of downstream steel scrap, rare earth scrap, and other metallic and non-metallic resources, building the company into a well-known enterprise in the circular economy sector. It will continue to advance the company's dual-wheel drive strategy, increase R&D, production, and sales of precision elevator parts, thereby building Weilman into a global industry leader in elevator signal systems and safety components; through fund operations, equity investments, mergers and acquisitions, and other capital operation models, accelerate the enhancement of the company's capital operation capabilities, achieve resource optimization and integration, continuously monitor extension opportunities in the upstream and downstream industry chain, and actively explore possibilities for the company's expansion into environmental protection, smart manufacturing, and IoT-related industries, forming new driving forces for company development and further enhancing its core competitiveness and profitability. According to the latest SMM price report: On July 17, the average price of Pr-Nd oxide was 766,000 yuan/mt, down 0.33% from the previous trading day. On July 17, Pr-Nd oxide futures prices declined, while inquiries in the spot market were sluggish. As a result, offers from Pr-Nd oxide suppliers edged lower. Nevertheless, most market participants remain confident about the outlook and showed a strong willingness to hold prices firm, which limited the actual decline in oxide prices, and low-cost supply remained scarce and hard to find. In the metals market, prices also fell. Magnetic material enterprises saw poor new orders, limiting their ability to accept high metal prices; purchases mainly served rigid restocking demand, leading to sluggish inquiries in the metal market. Upstream and downstream sectors remained locked in a stalemate, with the metals segment continuing to face pressure. In the short term, due to the stagnant trading, Pr-Nd product prices are expected to move sideways in a narrow range. Recommended Reading:

This is a summary. Read the full article at the original source.

Read full article at metal_news