Skanska Q2 2026 slides: record backlog offsets property writedowns

Skanska Q2 2026 slides: record backlog offsets property writedowns

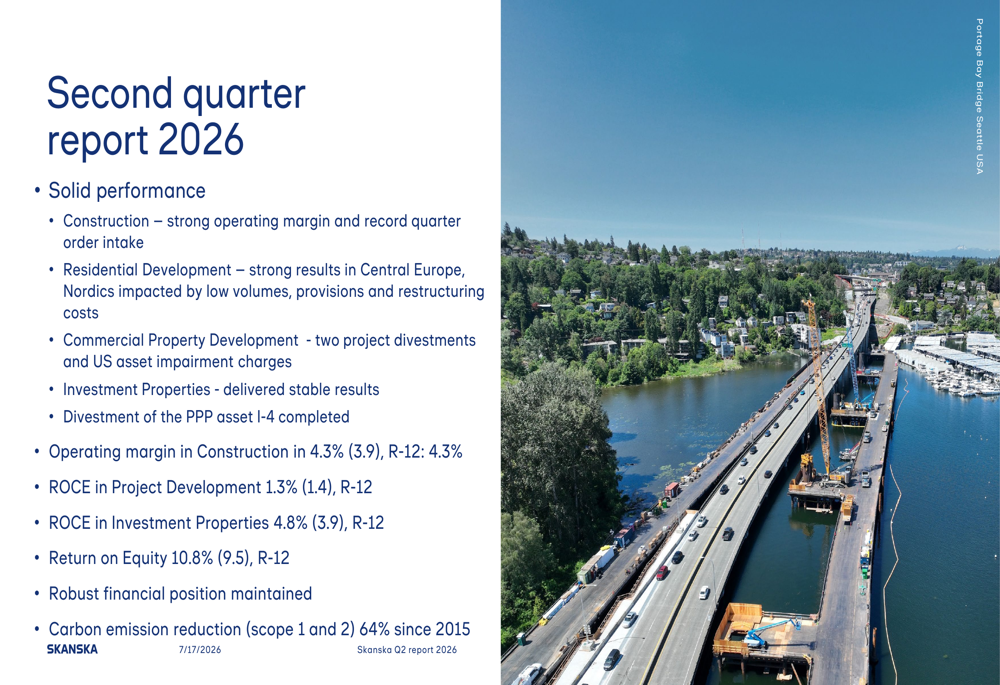

SpaceX selloff an ominous sign as lockup expiry looms Introduction & Market Context Skanska (STO:SKA-B) presented its second quarter 2026 results on July 17, 2026, revealing a company at two speeds: a construction business firing on all cylinders with record order intake, and property development operations grappling with market headwinds and asset impairments. Despite the construction segment’s historic performance, shares fell 3.01% to $246.70 as investors focused on weaker property-development earnings and SEK 464 million in U.S. commercial property writedowns. The Swedish construction and development giant reported an operating margin of 4.3% in its core construction business, matching its raised target level, while securing a quarterly record SEK 68 billion in order bookings that lifted its backlog to an all-time high of approximately SEK 300 billion. However, these achievements were partially overshadowed by a SEK 170 million operating loss in Commercial Property Development and sharply reduced profitability in Residential Development. Quarterly Performance Highlights As shown in the following overview of second quarter performance, Skanska delivered solid results in construction while facing headwinds in property development: The company’s return on equity reached 10.8% on a rolling 12-month basis, up from 9.5% in the previous period, while the return on capital employed in Project Development stood at 1.3%. Skanska also highlighted its environmental progress, achieving a 64% reduction in scope 1 and 2 carbon emissions since 2015. Construction Segment Strength The construction division remained the clear driver of Skanska’s performance, as illustrated in the following segment overview: Construction revenue held essentially flat at SEK 43.0 billion, but operating income rose to SEK 1,831 million from SEK 1,672 million in the prior-year quarter, pushing the operating margin to 4.3% from 3.9%. More significantly, the segment secured SEK 68.0 billion in order bookings compared to SEK 56.7 billion a year earlier, representing a quarterly record and lifting the order backlog to SEK 297.5 billion—also an all-time high. The book-to-build ratio reached 114% on a rolling 12-month basis, indicating robust demand conversion. CEO Anders Danielsson emphasized the momentum: "A record high order bookings of SEK 68 billion, which gives us a book-to-bill ratio of 114% on a rolling 12-month basis." The following chart illustrates the construction order bookings trend and the steady growth in backlog: Regional performance showed significant geographic divergence, as detailed in the following breakdown: The United States led with SEK 39.5 billion in orders, up from SEK 26.5 billion, achieving a 126% book-to-build ratio and maintaining 27 months of production visibility. The Nordic region posted SEK 24.2 billion in orders versus SEK 19.7 billion, with Sweden particularly strong at SEK 17.7 billion compared to SEK 9.6 billion a year earlier. Europe, however, saw orders decline to SEK 4.3 billion from SEK 10.5 billion, with a book-to-build ratio of just 94%. Operating margins by region showed the U.S. improving to 4.6% from 3.7%, while the Nordics held steady at 4.2% and Europe slipped to 3.5% from 4.0%. The following table provides the detailed regional breakdown: The construction income statement and margin trends demonstrate consistent profitability improvement: The rolling 12-month operating margin of 4.3% exceeded Skanska’s raised target of 4% or higher, with the gross margin expanding to 8.1% from 7.4% year-over-year. Property Development Challenges While construction thrived, Skanska’s property development businesses faced considerably more difficult conditions. Residential Development operating income plummeted to SEK 25 million from SEK 226 million in the prior-year quarter, with the operating margin collapsing to 1.5% from 11.3%. The following chart shows the residential development income trends and the sharp margin compression: The segment sold 352 homes compared to 409 a year earlier, while starts declined to 225 from 420. Revenue fell to SEK 1.7 billion from SEK 2.0 billion. Management attributed the weak performance to low volumes in the Nordics, provisions, and restructuring costs totaling approximately SEK 70 million. Excluding these charges, the underlying EBIT margin would have been 5.6%. Regional divergence was stark. Central Europe delivered a 22.9% operating margin on SEK 122 million of operating income, while the Nordic operations posted a negative 8.4% margin with a SEK 97 million operating loss. Sweden alone recorded a SEK 52 million loss with a -5.6% margin. Commercial Property Development reported a SEK 170 million operating loss despite generating SEK 217 million in gains from two project divestments. The segment was weighed down by SEK 464 million in asset impairment charges on several U.S. properties, reflecting valuation pressure from elevated long-term interest rates and macroeconomic uncertainty. The company maintained 17 ongoing projects representing SEK 12.8 billion in total investment and 16 completed projects worth SEK 18.5 billion with a 77% lease rate. Management indicated it would not rush to sell U.S. assets, preferring to wait for better market conditions while the properties continue generating cash flow. Investment Properties provided stability with SEK 85 million in operating income, up slightly from SEK 80 million, and maintained an 83% economic occupancy rate across its portfolio of seven high-quality office properties valued at SEK 8.3 billion. The following table details the segment’s comprehensive performance: Financial Position and Cash Flow Skanska demonstrated robust financial health with strong cash generation and a solid balance sheet. Operating cash flow from operations surged to SEK 7.1 billion from SEK 1.3 billion in the prior-year quarter, as shown in the following cash flow overview: CFO Pontus Winqvist noted that cash generation was supported by property deliveries and working capital improvement in construction. After accounting for dividends and net strategic divestments of SEK 5.9 billion, cash flow before changes in interest-bearing receivables and liabilities stood at SEK 1.2 billion. The company maintained available funds of SEK 23.1 billion, including SEK 7.0 billion in unutilized credit facilities. The following chart illustrates the maturity profile and funding composition: Interest-bearing net receivables improved to SEK 17.6 billion from SEK 12.0 billion a year earlier, while the equity-to-assets ratio stood at 37.1%. Total assets reached SEK 166.1 billion, with equity attributable to shareholders at SEK 61.7 billion. The following financial position summary provides additional detail: Capital employed in Project Development totaled SEK 63.4 billion, with Commercial Property Development representing SEK 40.4 billion, Residential Development SEK 14.8 billion, and Investment Properties SEK 8.2 billion. The following chart shows the investment and divestment activity: Market Outlook and Strategic Direction Management maintained an improved outlook for construction markets, citing robust demand in civil infrastructure across all geographies and strengthening conditions in building markets, particularly in Sweden and Finland. The U.S. market remains stronger than Europe, supported by investments in technology, industrial facilities, data centers, social infrastructure, and defense sectors. Danielsson highlighted the infrastructure opportunity: "We see a robust demand and good pipeline of projects for traditional infrastructure," pointing to the company’s strong position in the U.S. civil business and ongoing Congressional discussions about additional future funding beyond the current program. For property development, Skanska reiterated its 10% return-on-capital-employed target and emphasized discipline in project selection. "Our target is a 10% return on the capital employed in Project Development. That goes for RD as well, of course. We are not starting project if they doesn’t support that target," Danielsson stated. In Residential Development, the company is rebalancing its Nordic portfolio toward fewer cities and better-performing projects. Management acknowledged that recovery in Sweden, Norway, and Finland will take time, though Central Europe continues to show good activity levels with stable to increasing pricing. For Commercial Property Development, Skanska plans to continue deploying capital in Central Europe and the Nordics where business cases are stronger, while taking a patient approach with U.S. assets until transaction market conditions improve. Investor Response and Valuation Despite the record construction backlog and strong cash generation, Skanska shares declined 3.01% to $246.70, down $7.65 from the previous close of $254.35. The stock now trades about 12.3% below its 52-week high of $281.50 and approximately 10.2% above its 52-week low of $223.80. The market reaction suggests investors remain cautious about the volatility in property development earnings and the magnitude of U.S. writedowns, even as the core construction business delivers strong results. With a market capitalization of $10.6 billion, price-to-earnings ratio of 17.92, and dividend yield of 3.35% supported by 35 consecutive years of dividend payments, Skanska presents a mixed picture of operational strength tempered by development segment challenges. The company’s ability to maintain construction momentum while navigating the property development cycle will be critical to sustaining investor confidence in the quarters ahead. Full presentation:

This is a summary. Read the full article at the original source.

Read full article at investing_za